Cash flow keeps your business alive. When money in and money out do not match, stress rises and choices shrink. You may struggle to pay bills, cover payroll, or plan for growth. Careful planning can change that. You can use clear reports, steady routines, and simple rules to control timing and risk. Certified public accountants help you see patterns, avoid mistakes, and act early. They track what you earn, what you owe, and when each payment hits your account. They also help you prepare for taxes, slow seasons, and sudden costs. Through services like Corpus Christi accounting you gain structure and calm. You get honest numbers that guide every choice. This blog explains how CPAs support better cash flow management, so you can protect your business, your workers, and your own peace of mind.

Why cash flow matters more than profit

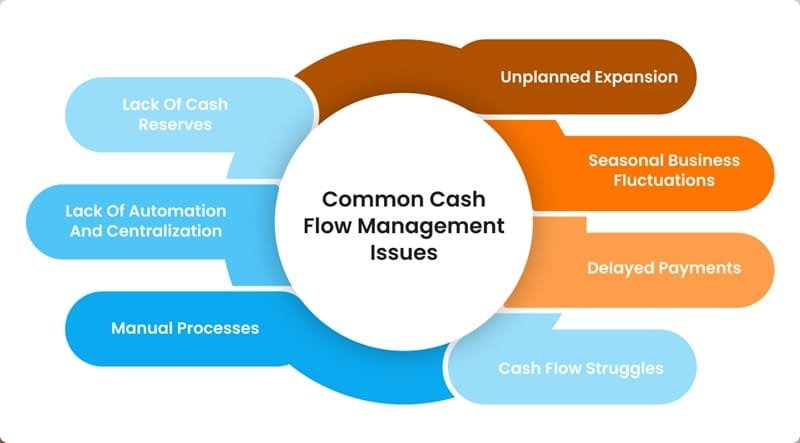

You can show a profit and still run out of cash. That surprise can break a young business. Cash flow is about timing. It shows when money enters and leaves your bank account.

You need cash to

- Pay workers on time

- Cover rent, supplies, and utilities

- Buy stock or equipment

Profit is a scorecard. Cash is fuel. When fuel runs out, work stops fast. A CPA helps you match your profit story with your cash story so you do not face that shock.

How CPAs track your cash the right way

Many owners watch only the bank balance. That view is not enough. A CPA builds a simple cash system that shows three things.

- What you already earned but have not collected

- What you already owe but have not paid

- What cash sits in reserve for trouble

First, you set up a cash flow statement. This report shows cash from operations, investing, and financing. The U.S. Small Business Administration explains these parts in plain language at https://www.sba.gov/article/2020/mar/02/how-create-cash-flow-statement. You use this report each month to see trends. A CPA keeps it clean and steady so you can trust it.

Planning ahead with a 13 week cash forecast

A short term cash forecast gives you a clear view. Many CPAs use a 13 week plan. That covers about one season of your business.

You list

- Expected cash in by week

- Expected cash out by week

- The net change in cash each week

You then spot weeks where cash drops too low. A CPA helps you move payments or collections to close those gaps. This stops panic and last minute loans.

Sample 4 week cash forecast

| Week | Cash in | Cash out | Net change | End balance |

|---|---|---|---|---|

| Week 1 | $20,000 | $18,000 | $2,000 | $22,000 |

| Week 2 | $15,000 | $19,000 | $4,000 | $18,000 |

| Week 3 | $25,000 | $17,000 | $8,000 | $26,000 |

| Week 4 | $12,000 | $20,000 | $8,000 | $18,000 |

This kind of table shows where you need a plan. A CPA helps you build and update it so it matches real life.

Using CPAs to control money in

Slow customer payments drain your strength. A CPA helps you tighten this part of cash flow with three steps.

- Clear invoices that show due dates and late fees

- Simple payment options like online pay and cards

- Regular follow up on late accounts

Next, you review which customers pay late again and again. You can change terms or ask for deposits. A CPA can show you how much cash you lose to late payments and help you set firm rules.

Using CPAs to control money out

Vendors want fast payment. You need balance. A CPA reviews your bills and finds three kinds of spend.

- Must pay now items like rent and payroll

- Can wait items where terms allow more time

- Can cut items that do not support your goals

You can then match each payment to your forecast. You might move some payments to steady your cash line. A CPA also checks if you use early pay discounts in a smart way or if those discounts hurt your cash.

Tax planning that protects your cash

Tax day should not be a shock. Large tax bills destroy cash flow. A CPA tracks your income and sets expected tax amounts aside during the year.

You work together to

- Choose the right business type for your tax load

- Plan purchases and write offs with care

- Use credits that match your work and workers

The Internal Revenue Service offers small business tax guides at https://www.irs.gov/businesses/small-businesses-self-employed. A CPA uses this guidance and shapes it to your case. That way you avoid both surprise bills and risky shortcuts.

Setting cash rules for a stable business

Good cash flow does not depend on luck. You need clear rules that you follow even during stress. A CPA helps you set three key rules.

- A target cash reserve, such as two or three months of fixed costs

- A review routine, such as a weekly cash meeting

- Simple triggers that force action, such as a low cash alert

You can also set family guards if you own a family business. You might agree not to pull cash out for big personal buys when the reserve is below target. A CPA can show how such moves would hit workers and long term plans. That view can calm tension at home and at work.

When to bring in a CPA for cash help

You do not need to wait for a crisis. You should reach out when

- You lose sleep over meeting payroll

- Your bank balance swings up and down each month

- You plan to grow, hire, or open a new site

A CPA gives you structure, clear reports, and honest feedback. You still choose your path. You just do it with open eyes and fewer shocks.

Cash flow can feel harsh, but you can control it. With a steady CPA partner, you protect your business, your workers, and the people at home who depend on you.